CMS has announced the official 2026 costs for Medicare Part A and Part B, including premiums, deductibles, and some coinsurance amounts. If you’re on Medicare now or about to enroll, here’s a simple explanation of what’s changing and what it might mean for your budget.

Medicare Part A: Hospital Coverage

Medicare Part A helps cover inpatient hospital stays, skilled nursing facility care, hospice, and some home health services. The good news is that about 99% of people with Medicare still pay no monthly premium for Part A because they worked (or had a spouse who worked) enough years and paid Medicare taxes.

For 2026:

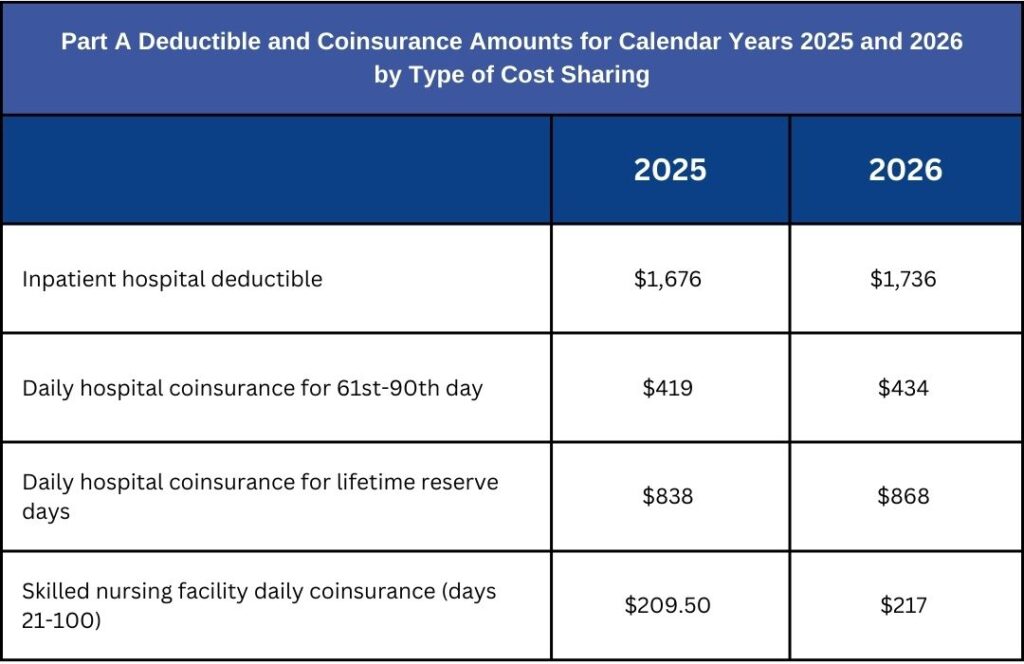

- Hospital deductible:

- When you’re admitted to the hospital, you’ll pay a deductible of $1,736 per benefit period (up from $1,676 in 2025).

- Hospital coinsurance:

- Days 1–60: $0 per day after you pay the deductible

- Days 61–90: $434 per day in 2026 (up from $419)

- After day 90: $868 per “lifetime reserve day” if used (up from $838)

- Skilled Nursing Facility coinsurance:

- Days 1–20: $0 per day

- Days 21–100: $217.00 per day in 2026 (up from $209.50)

If you don’t qualify for free Part A, your monthly premium will be:

- $311 per month in 2026 for people with at least 30 work quarters (or eligible spouse)

- $565 per month if you have fewer than 30 work quarters

Medicare Part B: Doctor and Outpatient Coverage

Medicare Part B covers things like doctor visits, outpatient care, lab tests, preventive services, and some medical equipment.

For 2026:

- Standard Part B premium:

- $202.90 per month (up from $185.00 in 2025)

- Part B annual deductible:

- $283 in 2026 (up from $257)

After you meet the deductible, you typically pay 20% of the Medicare-approved amount for most Part B services.

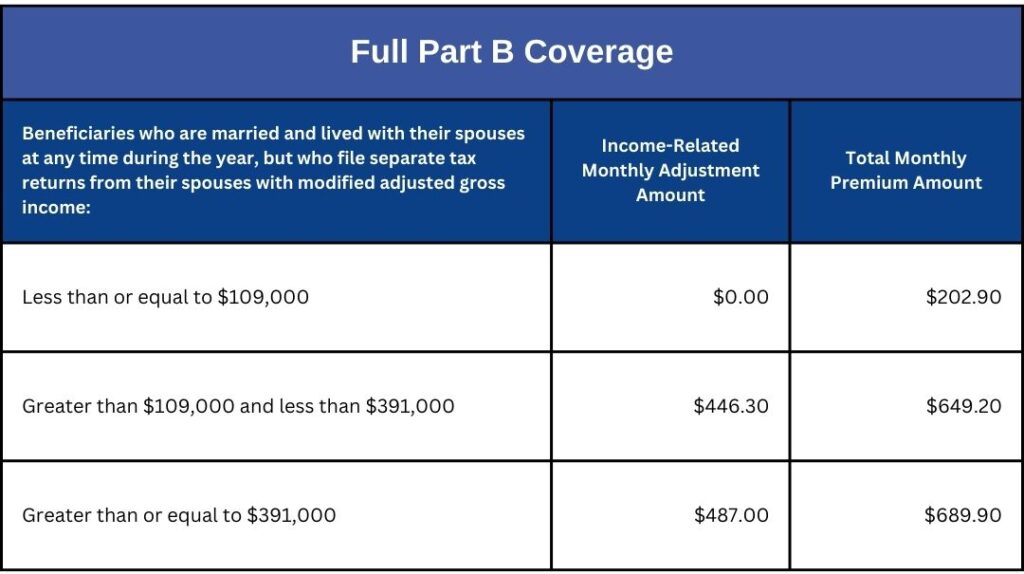

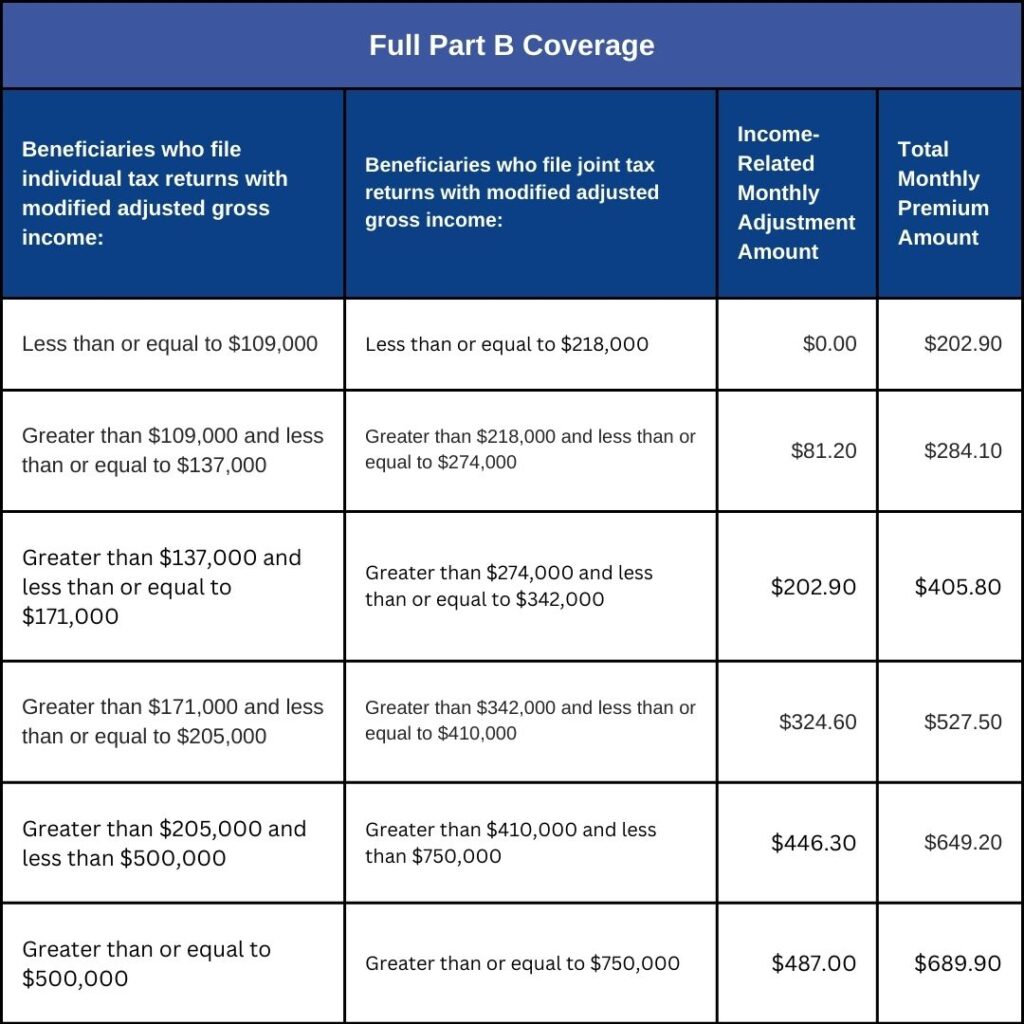

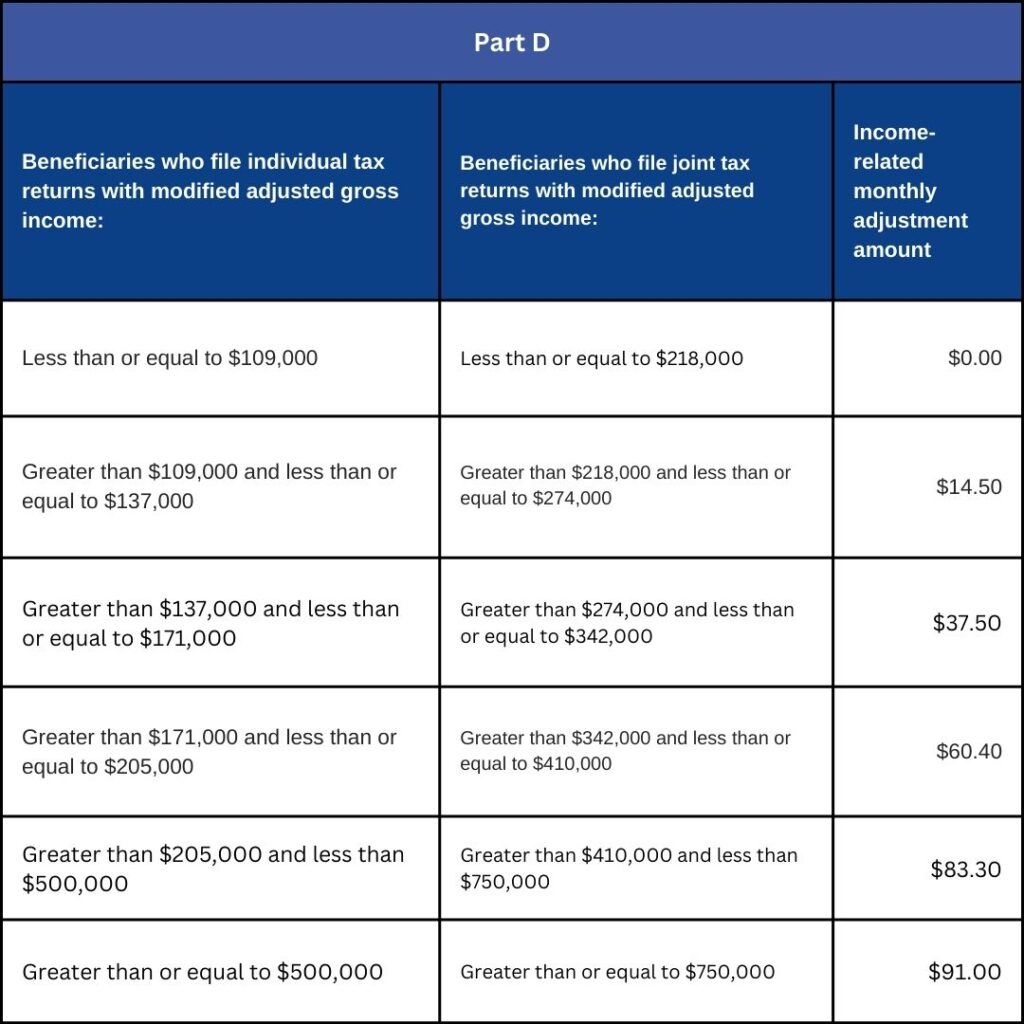

Higher-Income Beneficiaries: IRMAA

Some people with higher incomes pay more for Part B and Part D through what’s called an Income-Related Monthly Adjustment Amount (IRMAA). About 8% of people with Part B fall into this category.

If your income is below or equal to:

- $109,000 (single) or $218,000 (married filing jointly), you’ll pay the standard Part B premium of $202.90 in 2026.

If your income is higher than that, Medicare may add an extra amount to your Part B and Part D premiums. These surcharges are based on your IRS-reported income from two years prior and are listed in CMS’s official tables.

If you think your income has gone down significantly due to life changes (retirement, divorce, etc.), you may be able to appeal the IRMAA decision with Social Security.

What You Can Do Now

Here are a few practical steps to help you get ready for 2026:

- Review your current coverage.

Look at your Medicare Advantage, Medigap, and Part D plan to see how these new Part A and B amounts might affect your out-of-pocket costs. - Check your budget.

Build the new Part B premium and deductible into your 2026 healthcare budget. - Ask questions.

If you work with a licensed Medicare broker, they can walk you through how the new costs interact with your plan and help you compare options.

Medicare costs do change from year to year, but you don’t have to navigate it alone. The right guidance can help you stay confident and prepared.